LATEST INSIGHTS

Langham Hall supports Clipway on closing the largest-ever debut secondaries platform at $6.4 billion

UK Private REITs: Two years on

In April 2022, the UK implemented a new “private” real estate investment trust (‘REIT’) regime, which allowed fund managers to take advantage of the various benefits of REITs without having to undertake the more onerous listing requirement imposed since the beginning of the REIT regime in 2007. According to HMRC, there have been 29 private REITs set up since the regime was amended* and we expect to see the new regime continue to prove popular with fund managers as an alternative to using offshore structuring options.

What is a private REIT?

A REIT is a company limited by shares that invests in real estate, in order to primarily undertake property rental business. REITs are exempt from UK corporation tax on both income profits and capital gains, with tax being levied at shareholder level, meaning the tax impact on investors is similar to making a direct investment in the underlying real estate. This is particularly beneficial to tax exempt investors, such as sovereign investors or UK pension funds, who can claim exemptions on property profits received from a UK REIT.

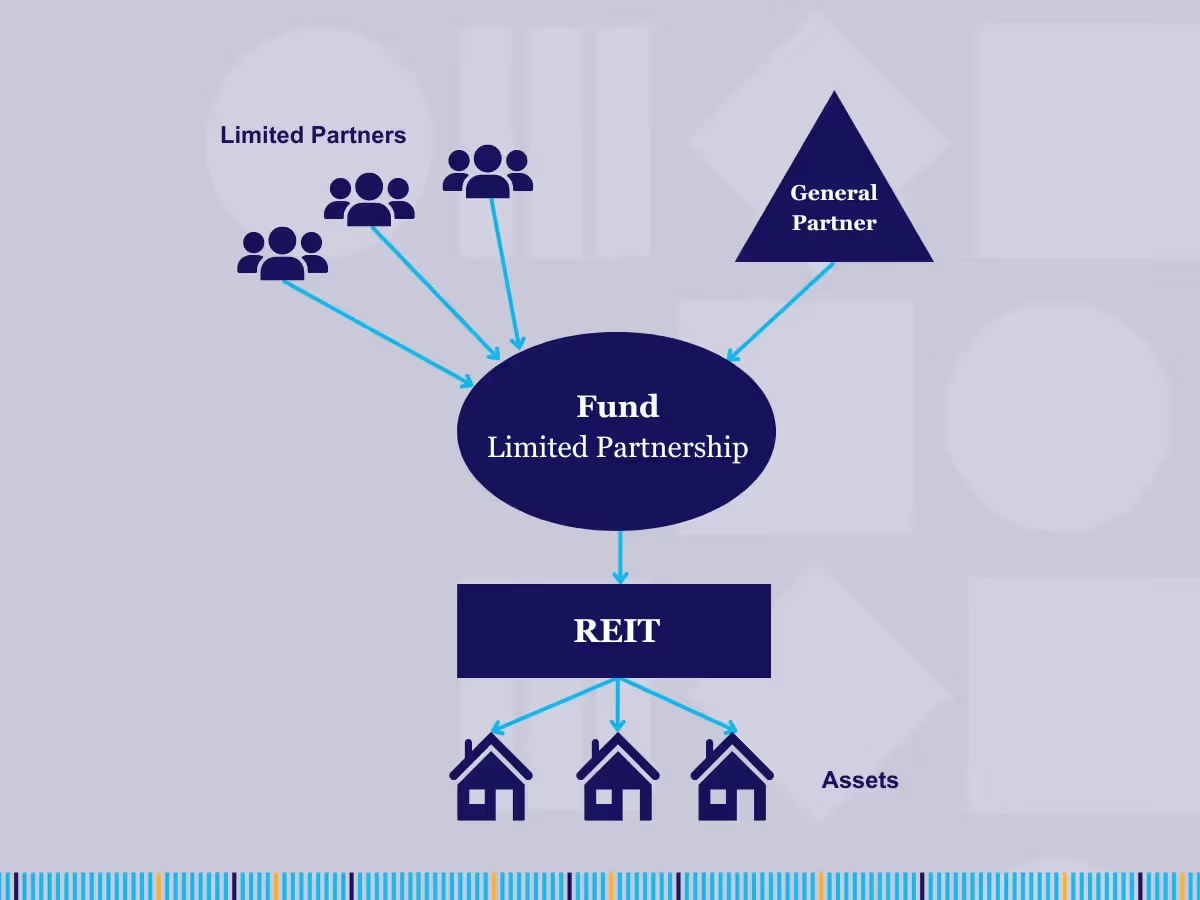

How is a private REIT typically used in a fund structure?

Traditionally, REITs were required to be admitted to trading on a recognised stock exchange, but the 2022 amendments have removed this requirement where at least 70% of the REIT’s ordinary share capital is held by institutional investors. Importantly, other commonly used fund structures (such as authorised unit trusts, or English limited partnerships) that meet a genuine diversity of ownership (‘GDO’) test are themselves considered an institutional investor for the purposes of the 70% test. Furthermore, real estate consultant John Forbes, who was consulted by HMRC on the GDO amendments, said that the rules on this have recently been made even more flexible, allowing ownership by parallel fund vehicles too. Using fund vehicles that meet the GDO test provides an attractive option for fund structuring, and in our experience a number of fund managers are exploring using a partnership structure to admit investors, with a private REIT held directly beneath.

This type of structuring has been commonly used elsewhere, for example in the US, for many years now, so is well understood by global institutional investors.

What are the requirements to hold REIT status?

To maintain private REIT status, managers should be aware of several conditions that must be met for a company to qualify for and continue to hold REIT status, including but not limited to;

- Property Income Distribution (‘PID’): a REIT is required to distribute no less than 90% of its property rental income as a dividend. This income is not taxable at the REIT level but is subject to withholding tax on distribution. Any other profits (e.g. interest receipts or property trading profits) are subject to UK corporation tax. Generally, an experienced fund administrator will work closely with a specialist tax advisor to ensure compliance with the PID requirements.

- Close company test: Companies are considered “close” if controlled by five or fewer participants This is not permitted for REITs. However, the new regime allows REITs to be close for the first three years and can be close if held by an institutional investor.

- Property business: a REIT must hold at least three properties, with no single property representing more than 40% of the value of the REIT. The exception to this rule is where the REIT owns at least one commercial property valued at £20 million or more.

Operational considerations

The PID calculation is, in our opinion, one of the most important elements of running a private REIT. Failure to distribute enough of property income can result in a company potentially losing REIT status, and instead being subject to 25% UK corporation tax. Using an experienced fund administrator in conjunction with a specialist tax advisor minimises this risk.

Additionally, private REITs are also required to submit a quarterly CT61 return for each period in which a PID is paid, and a reconciliation for each accounting period of how distributions made in that period have been attributed. Again, working with a fund administrator that has experience in the operation of these structures is important here.

Finally, there is a “Holder of Excessive Rights” charge levied on any shareholder which is beneficially entitled to 10% or more of dividends or voting rights of the REIT, meaning a tax charge will be imposed on any distributions made to such a shareholder. The new regime relaxes this rule for shareholders who are entitled to gross payment of distributions, such as UK corporates and pension funds, allowing them to avoid having to fragment their shareholdings by use of multiple SPVs.

What next?

We expect to see a continued growth in the use of private REITs for holding income producing real estate in the UK, particularly as so many public REITs continue to trade at deep discounts to NAV. The ability to use a private REIT within a wider fund structure makes for an attractive option to fund managers and makes the UK increasingly attractive as a fund domicile. A private REIT may also be a good stepping stone to a listed REIT later. A pool of assets can be built up when the REIT is private with the REIT then being listed via an IPO at a more propitious point in the market.

Operating such structures comes with complexity, and we would urge anybody considering the use of a private REIT to speak to us about the operational aspects of running such a structure.

* As at 31 Jan 2024. Confirmed via a Freedom of Information Act request submitted directly to HMRC

Langham Hall charity initiatives – 2023 wrap-up

Langham Hall is committed to giving back to the communities in which it operates. We champion our staff to be involved in a variety of activities to widen their life experiences and perspectives.

During the second half of 2023, our global offices challenged themselves with a range of charity and fundraising activities.

We looked back at their successes:

Jersey

Jersey continued their support for their chosen charities Jersey Hospice Care and Dementia Jersey.

They started the second half of the year by donating their monthly dress down collections to both the charities.

The office also took part in The Jersey Hospice Care Dragon Boat Racing (coming 7th!) as well as sponsoring the Santa Dash for the second year in a row.

They ended the year by manning the Dementia Jersey stall in town as well as helping wrap presents ahead of the festive season.

In total they raised £3,140 for Jersey Hospice Care and £1,000 for Dementia Jersey.

Guernsey

The second half of 2023 was a busy period for the Guernsey team. In July a group of six employees (and one dog) joined in the Gower Walk of Hope in aid of Guernsey Mind. August saw a bake sale and the Tower to Tower Walk and Run, both in support of Guernsey Alzheimer’s Association.

A team of five colleagues entered the Skipton Swimarathon in October swimming a very impressive 160 lengths in aid of Guernsey Mind and the Guernsey Youth Commission.

The team ended the year taking part in Beard Up! Challenge for local charity Male Uprising Guernsey whose aim is to raise awareness of male cancers and general wellbeing in the Bailiwick of Guernsey.

UK

The London office took part in Movember, where participants were set the challenge to either grow a moustache or aim to move 60k across the month, to represent the 60 me who commit suicide across the globe every hour. Thanks to their brilliant efforts the office raised over £2,700.

The team closed the year taking part in Christmas Jumper Day, which saw the office wear a fantastic selection off knitwear while raising over £350.

The office also made donations on behalf of the business and staff.

- Assistance with the Moroccan Earthquake relief efforts

- Assistance with the Libyan flooding relief efforts

- Donations to Motor Neuron Disease Association and Zarach (staff chosen charities)

Luxembourg

The Luxembourg office marked Breast Cancer Awareness month in October by designating two days of the month as ‘Pink Days’. Staff were encouraged to wear something pink and share a picture. Donations were made for every participant.

The team also assembled and joined the corporate football league organised by Social Goal, an NGO dedicated to making a positive impact for underprivileged children from diverse communities and cultures with the money collected by promoting employee well-being, engagement, and networking through corporate sports experiences.

The office rolled out an initiative to contribute to the wellbeing of others by donating blood or plasms to the Red Cross at any time, including working hours.

Colleagues also took part in Movember as well as matching employee contributions for the Moroccan Earthquake relief.

Asia

The Hong Kong office organised a steam workshop at The Hub HK. The charity provides support to families from disadvantaged backgrounds whose children needed to be taken care while their parents are at work. The centre provides support for children’s educational, physical and mental development.

We also encourage our staff across all jurisdictions to take on their own challenges and initiatives.

- Paul Tsang from London took part in the RNLI Tower Run

- Joseph Dennis from London took part in the Hever Castle Triathlon raising money for Macmillan Cancer Support

We look forward to all the different initiatives the teams have planned for 2024.

We are proud to stand together and extend a helping hand to those in need.

Join our newsletter

By subscribing you agree with our Privacy Policy